The Climate Imperative

Limiting global warming to 1.5°C above pre-industrial levels is not merely a climate target; it is a lifeline. It could shield 1.7 billion people from extreme heat, prevent the displacement of 280 million people due to sea level rise, and halve the risk of species extinction compared to a 2°C trajectory. It also offers the best chance to limit climate-induced disasters such as droughts, floods, and food insecurity.

However, current global pledges are off track. Projections suggest a temperature rise of 2.6°C to 3.1°C by 2100, with the 1.5°C threshold potentially breached as early as 2028. Urgent, scalable, and commercially viable action is required.

The stakes of inaction are clear if we keep on our trajectory of 2.8°C:

74% of the global population is exposed to deadly heat waves every year, resulting in millions of deaths

Over 3.3 billion people (40% of the global population) are exposed to multi-hazard climate risks

Global crop yields (wheat, rice) decline 20% to 40%, and food prices soar

Sea levels rise by c.1m by 2100, Coral reefs all collapse, and the sea will continue to rise to c.3m

30% to 50% of species lose their habitat and are vulnerable to extinction

On this trajectory, climate change will be overwhelming and destabilising; it will devastate the poorest nations and affect everyone on the planet. It’s a future we must avoid! However, the world is falling short. Without more decisive action, the 1.5°C threshold may be crossed within just a few years. To alter this course and accelerate change, the energy transition must be commercially viable. It must improve business performance rather than hinder it.

Targets and Progress

The UK Paris Agreement

68% reduction in emissions by 2030

1) The UK’s Nationally Determined Contribution (NDC) for the Paris Agreement is to reduce emissions by 68% below 1990 levels by 2030.

By 2030 the UK needs to be 68% below 1990 level of 822 MtCO₂e = 263 MtCO₂e.

As of 2024 we are currently at 414 MtCO₂e. That means that we need an additional 36% cut from today’s emissions in just 6 years, which means we need to increase from a CAGR reduction of 2.5% (2022 to 2024) to 7.1% (2024 to 2030), i.e. triple our speed reduction (see graph below)

The Clean Power Act

100% of Electricity demand from Clean Power” by 2030

2) The Clean Power 2030 Action Plan aims for 100% of electricity demand to be met by “clean power” in a typical year.

Of that clean generation, at least 95% of domestic electricity generation should come from low-carbon sources (wind, solar, nuclear, biomass), with no more than 5% from unabated gas (gas without carbon capture).

Over the last 12 months, Clean / low-carbon electricity from wind, solar, nuclear, biomass, and hydropower accounted for about 57% of electricity generation, and the share from fossil fuels fell to 31.8% (mainly unabated gas); the rest is typically exported. In August, zero-carbon sources, wind, solar, nuclear, and hydro reached 62%. The split of the energy sources can be seen in real time by looking at the GB energy dashboard (as seen below)

Simply put, the trend is in the right direction: fossil share, especially of unabated gas, is falling. Clean sources are growing. However, the current pace of 4% is not yet fast enough to meet the 2030 Clean Power target as the pace needs to increase to 8.8% to deliver the target.

As you can see in the graph above, in 2010, there was low renewables penetration, and nuclear was the bulk. By 2015, there was a significant expansion of wind, solar, and biomass, with the low-carbon share jumping to 45%. 2020 saw a record in renewable energy output, with coal almost eliminated, and COVID-19 reducing demand. In 2021, the low-carbon electricity dropped due to unusually low wind output and more gas generation. In 2022, wind recovered somewhat, but nuclear outages reduced its share. In 2023, renewables continued to grow but gas didn’t change much. In 2024, gas usage began to decline, with renewables increasing to 50.4% and nuclear energy at 14.3%. 2025 is not yet complete, but mid-year results suggest a slight dip due to lower wind/solar output due to weather and nuclear outages. In 2024, c.66% of the UK’s electricity came from low-carbon sources (renewables + nuclear). Renewable share wind + solar + hydro is about 36% for electricity generation. Fossil fuel sources, gas use is lower and coal has ceased within electricity production

UK Electricity Generation from Solar Power

45 to 47 GW by 2030

3) The UK government has set a target of 45–47 GW of installed solar PV capacity by 2030

This under the Solar Roadmap and the Clean Power 2030 plan, compared to around 15 GW operating today. This target combines both ground-mounted and rooftop projects, with the government highlighting that 9 to 10 GW could come specifically from smaller-scale rooftop solar (commercial, industrial, and small ground-mount) by the end of the decade.

Recent deployment has been steady but modest: the UK added around 1.1 GW per year in 2022 and 2023, equivalent to around 6% compound annual growth rate since 2020. To meet the 2030 target, however, this growth rate needs to accelerate sharply to around 18% CAGR, requiring annual additions of 3 to 4 GW per year.

Government analysis emphasises the role of rooftop projects that do not trigger large Transmission Impact Assessments, as these can connect more quickly and avoid lengthy grid upgrade delays. If the roadmap is achieved, solar generation would rise from today’s c.16 TWh per year to 40–45 TWh by 2030, providing a significant share of low-cost, distributed electricity close to where it is consumed.

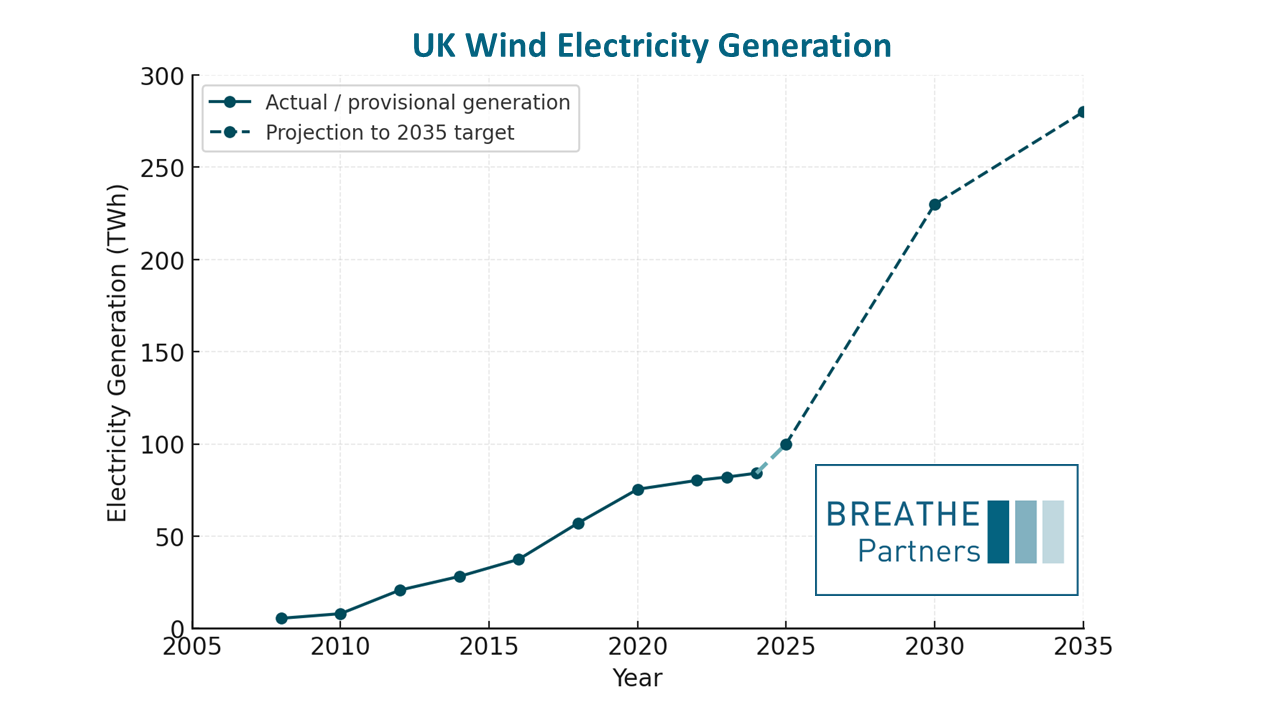

UK Electricity Generation from Wind

70 to 80 GW by 2030

4) The UK government has set a target of 50 GW offshore wind capacity by 2030 as part of the British Energy Security Strategy and the Clean Power 2030 plan, alongside ambitions for 30 GW of onshore wind. Together, this would bring UK total wind capacity to around 70to 80 GW by 2030, compared to 32 GW today.

Within this, onshore wind is expected to play a significant role: recent reforms in the Energy Security Act (2023) are intended to make planning for onshore turbines in England easier, though devolved nations (Scotland, Wales, Northern Ireland) already account for the bulk of UK onshore growth. Offshore wind remains the cornerstone, with more than 13 GW of projects under construction and 80 GW is in the development pipeline, according to DESNZ.

The UK added 3 GW of wind capacity in 2023 (mainly offshore), representing a c.10% CAGR since 2010. However, to meet the 2030 targets, additions need to accelerate sharply: an average of 6 to 7 GW per year, or nearly double the current pace. If the pipeline is delivered, annual wind generation could increase from today’s c.85 TWh to around 200 to 250 TWh by 2030, covering more than half of UK electricity demand.

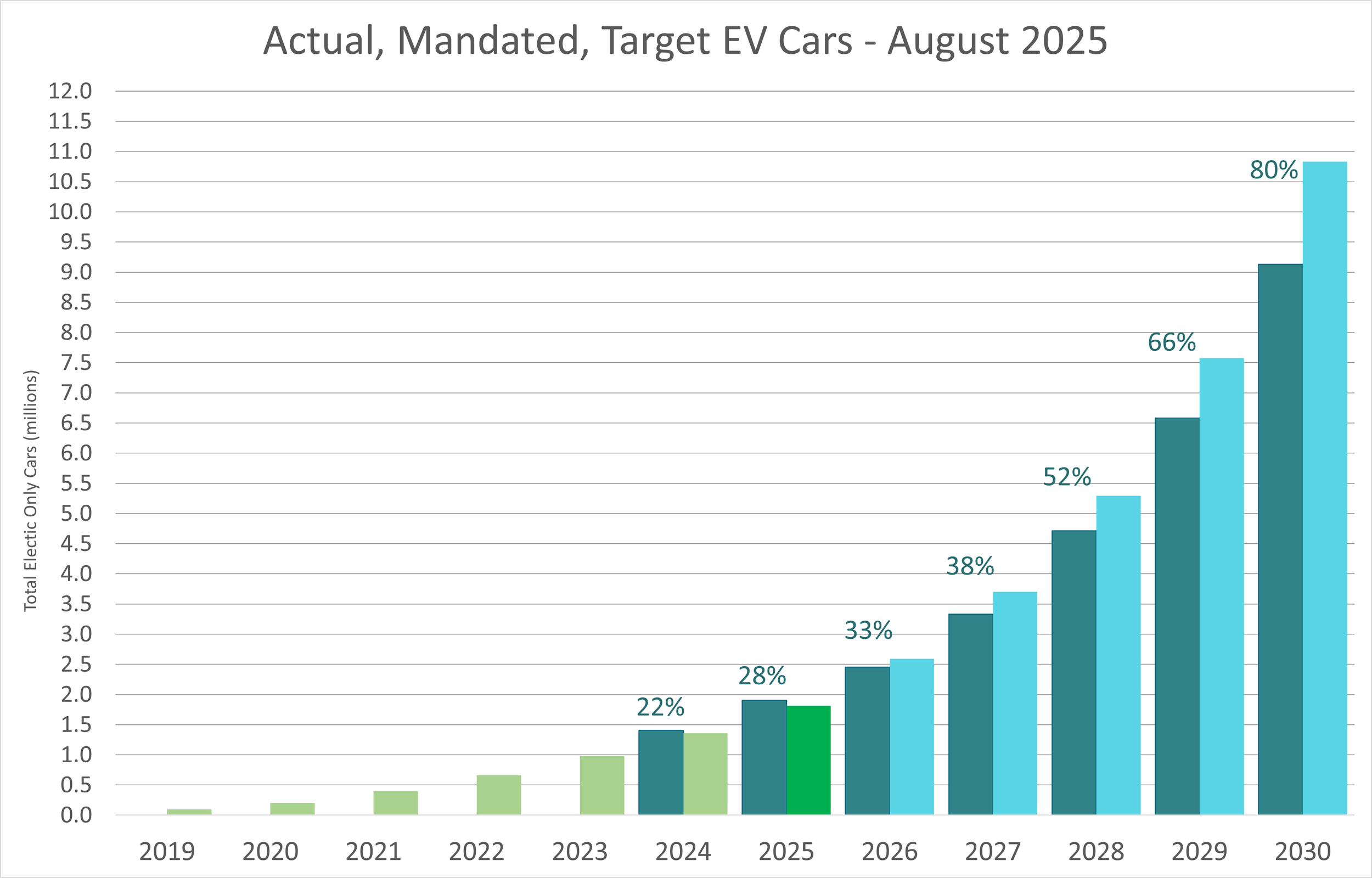

Electric Vehicle Mandates for new cars and vans

11m EV Cars, 1.5m vans and 30k HGV’s by 2030 (Breathe estimate)

5a) Electric Cars

By 2030, we anticipate there will be around 10.8 million electric cars on UK roads (±10%), representing 35% of all vehicles compared to just 5% today. This projection builds on rapid recent growth: from only a few thousand EVs in 2010, the fleet expanded to more than 1.2 million by 2022, with over 1.1 million additional sales in the past three years alone, equivalent to a compound annual growth rate of around 40%.

Economically, shifting company cars from petrol/diesel to electric could save £9.8 billion annually by 2030, while cutting energy demand by 66 TWh.

The acceleration reflects a mix of regulatory and market levers. The 2030 ban on new pure petrol and diesel cars, the Zero Emission Vehicle (ZEV) Mandate (which steadily increases the required share of new electric sales as shown in the graph), and supporting flexibilities such as borrowing allowances and car and van credit transfers are driving supply.

There are also regulations and financial incentives, including favourable Benefit-in-Kind rates for company cars, ongoing plug-in grants for vans and taxis, and government-backed charging investment through the LEVI fund. These are helping to de-risk adoption and build consumer confidence.

Looking forward, by 2035, when all new cars must be zero-emission, the EV fleet could plausibly exceed 20 to 22 million cars, equating to more than half of all cars on the road, provided current policy is maintained and charging infrastructure deployment keeps pace.

5b) Vans

By 2030, we expect around 1.5 million electric vans on UK roads (±15%), up from 89,718 electric vans today (16,365 new electric vans YTD). This would take EV vans from just 1.8% of the fleet now to a significant share within the decade. Growth is being driven by the Zero Emission Vehicle (ZEV) Mandate, which requires 70% of new van sales to be zero-emission by 2030 and 100% by 2035. Current uptake is modest, with 8.4% of new van sales being electric. Still, the trajectory is reinforced by regulatory flexibilities, manufacturers can borrow against future targets, trade credits between vans and cars, and offset some compliance using CO₂ reductions from non-ZEVs. Exemptions also apply for small-volume manufacturers until 2030 or 2035, mirroring the car framework. On economics, switching vans from diesel to electric would cut annual operating costs by around £9 billion in 2030, while saving 64.8 TWh of energy demand

5c) HGV’s

All new HGVs under 26 tonnes must be zero-emission by 2035, with all heavier HGVs following by 2040. Adoption is still at an early stage; just 1,271 electric HGVs are currently in operation out of a total fleet of 626,000 (0.2%). However, based on policy trajectories and early deployments, we project that the zero-emission HGV fleet could grow to around 30,000 by 2030, over 120,000 by 2035, and as high as 300,000 by 2040 (approaching 50% of the fleet). Transitioning HGVs to electric would save operators around £8 billion annually by 2030, while reducing energy demand by 60 TWh compared to diesel. Delivering this scale-up will require significant investment in depot charging, grid upgrades, and potentially hydrogen refuelling.

The Zero Emission HGV and Infrastructure Demonstrator (ZEHID) programme is the government’s flagship to de-risk this transition. Backed by over £200 million, ZEHID is funding large-scale trials of battery-electric and hydrogen fuel-cell trucks alongside megawatt-scale depot and public charging/refuelling infrastructure. These demonstrations, which are expected to run into the end of the decade, are designed to prove technical feasibility, reduce cost uncertainty, and build operator confidence, helping to ensure that the 2035 and 2040 targets are both technically and commercially achievable.